From $350 to $1,250 a Month: The North Carolina HOA Story Every Buyer Should Read Before Closing

A subdivision near Charlotte raised HOA dues from $350 to $1,250 a month and added a $10,000 special assessment. The viral outrage misses the part that should actually worry buyers, and the part you can check before you sign.

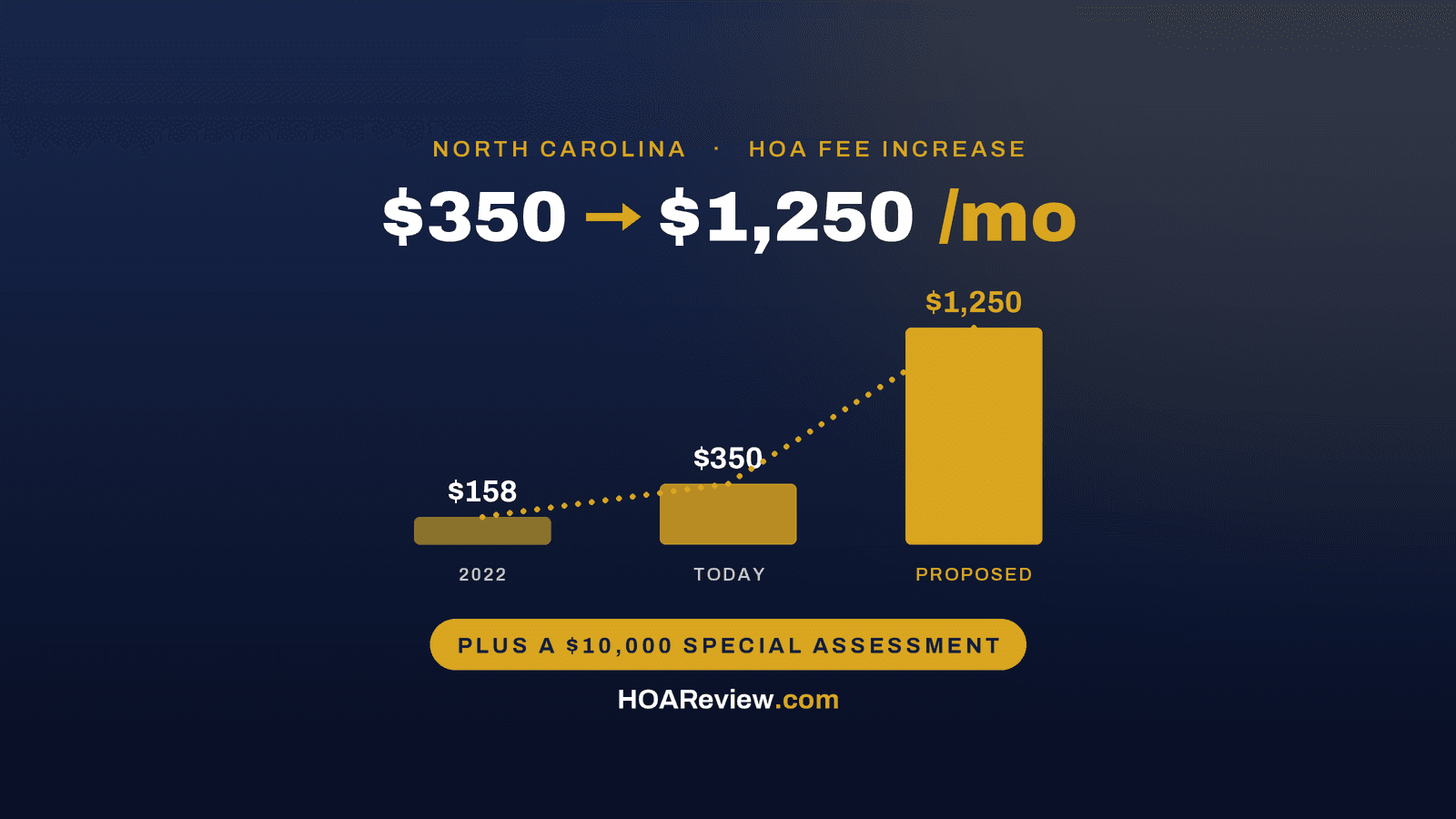

A homeowners association near Charlotte just raised monthly dues from $350 to $1,250 and tacked on a $10,000 special assessment. The story went viral this week, and the reaction was about what you would expect: shock, anger, and a wave of "this is why HOAs should be illegal."

The anger is understandable. It also skips past the part that matters most if you are about to buy a home. Almost everything that blindsided these owners was knowable before they closed. That is the real lesson, and it is the reason this site exists.

Here is what happened, what is actually driving it, and exactly what to pull before you buy into any community with an association.

What the reporting says

According to WSOC-TV in Charlotte, homeowners in the Magnolia Cove subdivision in Sherrills Ford, in Catawba County on the Lake Norman side of the metro, are facing dues jumping from $350 to $1,250 a month, plus a one-time $10,000 special assessment. Residents told the station the dues were $158 a month four years ago. Several said the fees were supposed to cover lawn care and a community pool that was never built.

Residents also said the developer is the president of the HOA, that many of the homes in the neighborhood are now rentals, and that they are not being allowed to vote on the increases. The next association meeting is being held virtually, with questions required in advance.

The association is not silent on this. Its attorney told Channel 9 the assessments are being raised to properly fund the association's operations, and that the developer covered shortfalls for years because a large number of owners were delinquent or simply not paying. Litigation is already underway, so the facts here are contested and a court may sort out who is right. We are not treating the residents' account as proven. We are using it to explain a structure that is very real and very common.

How a developer still runs the HOA after people have moved in

This is the part that confuses people, and it is worth understanding because it is not a loophole. It is how these communities are built.

When a developer creates a subdivision, the governing document, called the declaration, almost always reserves a period of "declarant control." During that window the developer appoints and removes the board. That is normal, and it is supposed to end once enough homes are sold.

But control can outlast that window for a second reason: votes usually attach to lots, not to people. If the developer still owns most of the lots, the developer still holds most of the votes, and therefore still elects the board and still sets the budget. A community where the builder kept a large share of the homes and rented them out, instead of selling them, is a community where the builder can keep voting control long after the first families move in. Twenty owners do not outvote an entity that holds the majority of the lots.

So when residents say they "cannot vote it down," the underlying math is often simpler than a conspiracy. North Carolina law actually does give owners a budget ratification vote, and a proposed budget is rejected only if a majority of all lot owners vote it down. If one party controls the majority of lots, that majority is out of reach for the remaining owners no matter how the meeting is run.

The line buyers should focus on: "you take a loss"

The viral version ends with a warning: if you sell, you take a loss, and the special assessment still has to be paid. The instinct is right. The usual explanation for it is wrong, and it is worth getting this correct.

A special assessment in North Carolina is the lot owner's obligation, and it can become a lien on the home if it is not paid. At a sale it generally has to be cleared. So yes, the $10,000 follows the house until someone pays it.

The bigger driver of a loss is the carrying cost. Lenders count HOA dues against a buyer's debt-to-income ratio. At roughly today's mortgage rates, $1,250 a month in dues consumes about the same monthly budget a buyer would otherwise put toward $185,000 to $190,000 of mortgage. In other words, the dues alone erase a large chunk of what any buyer can afford to pay for the house itself. That shrinks the buyer pool and pushes the price down. Add a pending lawsuit, which makes buyers nervous and can complicate financing, and an appraiser who will factor in the instability, and you get exactly the loss the post describes.

One myth to retire, because you will see it repeated in the comments: people will tell you a neighborhood full of rentals automatically makes homes impossible to finance. For condos, that owner-occupancy and investor-concentration cap was actually eliminated by Fannie Mae and Freddie Mac in March 2026. For a subdivision of single-family or townhomes, those condo rules generally never applied in the first place. The rental share is a yellow flag about who controls the community and where it is headed. It is not, by itself, the thing that blocks a mortgage. Pending litigation and weak association finances are.

Could a buyer have seen this coming? Mostly, yes

Not the exact dollar figure. But the shape of this was visible. A community still controlled by its developer, a large and growing share of rentals, an amenity that was promised and never delivered, reserves that were clearly not keeping up. Those are not secrets. They are documented in the association's own records, and a buyer is entitled to them.

The problem is that they are scattered across the declaration, the bylaws, the budget, the reserve study, the meeting minutes, and the resale disclosure, and most buyers never see them until they are already under contract and emotionally committed.

What to pull before you buy into any HOA

If a home you are considering has an association, request these and actually read them. A good agent can get most of them, and in North Carolina you are owed a resale disclosure.

- The declaration and bylaws. Look specifically for the declarant control provisions and how votes are allocated. If the developer still controls the board, know that going in.

- Who owns the lots, and how many are rentals. A high or rising rental share, especially concentrated in one owner, tells you who really runs the place.

- The last two or three annual budgets. A steep dues trajectory is the single clearest warning. Going from $158 to $350 in four years was already a signal.

- The reserve study and reserve balance. Underfunded reserves are how a "surprise" $10,000 assessment gets built. The money has to come from somewhere.

- Special assessment history and any planned assessments. Ask directly, in writing.

- Pending or threatened litigation. This affects both your peace of mind and your financing.

- Meeting minutes. Unbuilt amenities, deferred maintenance, and owner complaints usually show up here first.

If the answers are hard to get, or the board will only take questions submitted in advance for a virtual meeting, treat the friction itself as information.

North Carolina lawmakers are weighing bills to limit HOA power, and reform may eventually change some of this. It will not change in time for anyone closing this month. The protection that works today is doing the homework before you sign.

The real problem, and what we are building to fix it

None of this information is hidden, exactly. It is just fragmented, buried in documents you only get late, and impossible to compare across communities. That gap is precisely what catches buyers by surprise after closing, and it is what HOAReview exists to close. We index HOA communities so you can see fees, history, management, and resident experiences in one place, before you make an offer, instead of discovering them in a letter after you move in.

Before you fall in love with a house, look up the community. Thirty seconds now is cheaper than a $1,250 surprise later.

Search your community at HOAReview.com

This article is based on reporting by WSOC-TV in Charlotte. The dispute described is the subject of ongoing litigation, and the allegations have not been resolved. This is general information for home buyers, not legal advice. For a specific situation, consult a licensed North Carolina attorney.